There is an economic principle called ‘diminishing returns’. This says, in effect, that your first hamburger is great, the second OK, but by the time you are on to your third and fourth, the returns in terms of enjoyment and allaying hunger are greatly diminished. Continue and the returns will eventually become negative. Of course, long before you become physically ill, the benefit:cost ratio will itself have become negative. This does not only apply to hamburgers. It applies to everything, including our policy settings. For a while the benefit of the new policy outweighs the disadvantages – until it doesn’t. We often fail to see the change because we are always looking backwards – justifying our current actions by the gains we have already made, and asssuming that these gains will continue.

Consider that over the last several decades we have made great efficiency gains in infrastructure services such as electricity production and distribution by increasing the size of our production units and integrating our networks. There was a period (up to about the late 1980s) when it was always more efficient to build a new plant rather than renew an ageing one because technological improvements were increasing boiler size resulting in vastly reduced capital costs and considerable savings in labour.

Eventually two things happened. The technological gains slowed down. And risks increased. For one thing, if you can satisfy demand with 6 units of a given size, should one fail you have lost 1/6th of your total output. But when the size of units increases to the stage where total demand can be satisfied by just 3 units, then failure of just one unit reduces your capacity to serve by 33%. Gains slow down, risk costs rise. We can see a similar pattern in the integration of networks. Initially the gains are great, and obvious. We do more integration and we get further gains. But the more individual networks that are connected the greater the risk that an accident in, or mismanagement of, any link in the chain will have flow on effects to the others.

And so we get events such as the 2003 major blackout of the NorthEast of America which extended into Canada and, closer to home, the 2016 widespread power outage in South Australia that occurred as a result of storm damage to electricity transmission infrastructure. The cascading failure of the electricity transmission network resulted in almost the entire state losing its electricity supply. To add to our worries are recent accounts of Russian hacking into US nuclear power plants.

So big is not necessarily beautiful. But what’s the alternative?

Today’s post is by Jeff Roorda, Technology One, and Deputy Chair of Talking Infrastructure.

Is using condition to determine life a fundamental error in asset registers?

Part 1

How long does an asset last? The answer determines life cycle cost, depreciation and infrastructure planning.

Asset registers estimate useful life for every asset but which life do we use? The physical life or the economic life? Yes these are different, and often materially different. I recently was working in Queenstown NZ with Queenstown-Lakes District Council. After work, I boarded the steamer TSS Earnslaw that had been carrying passengers on lake Wakatipu since 1912, and its steam engine is still powered by coal. The Earnslaw and many steam powered transport assets around the world still have many years of remaining physical life after over 100 years of operation.

So why did we stop using steam for transportation ? Was it because the assets reached their physical life?

In hindsight we all know the answer. Because steam power is dirty and technology made steam power obsolete. OK then, so the economic life was determined by function and capacity, not by physical condition. Even though steam powered assets had many years of physical life remaining, they became obsolete relatively quickly, far more quickly than most people managing the assets predicted. How much of the infrastructure we are building right now will be obsolete well before physical life is reached? So why do we focus on the measurement of physical life using condition instead of function and capacity? The pace of change could be faster now than in the 1940’s and 1950’s when transport shifted from steam to the internal combustion engine which created the infrastructure networks we now manage.

Think about what we are building now and drivers for change.

Infrastructure based on continuing the past where everyone has to travel to the office at the same time creating peak transport loads using internal combustion engines with one person per car does not seem to be a likely future with changes in communications and energy technologies.

Part 2 coming shortly.

Just over a year ago (Jan 6 2017), I wrote about ‘Pop Up’ Prisons, more accurately called ‘rapid build’. Rapid build is used in war zones where there is a sudden and urgent need. It is extremely expensive. Overcrowding of our prisons had led to this now being considered an urgent need, but why had we not foreseen it? One answer had, in fact, been earlier suggested by Mark Neasbey in his post “Infrastructure decisions we make when we don’t think we are making any”(Aug 12 2016) where Mark had brilliantly, and entertainingly, explained how the ‘costless’ decision to put more police on the streets to combat crime had cost consequences which were not only extensive, but, unfortunately, invisible in the eyes of decision makers.

Now, today, comes news from America where incarceration rates have increased 500% over the last few decades. Philadelphia in Pennsylvania is even more extreme, their incarceration rates have increased 700% in the same time. But that is already changing with the appointment a few months ago of a civil rights lawyer, Larry Kranser, as the new District Attorney who is taking extreme action to reduce the cost and human damage involved. The whole encouraging story can be found on the Slate website here but I would like to draw your attention to one move which could effectively be used more widely.

“In a move that may have less impact on the lives of defendants, but is very on-brand for Kranser, prosecutors must now calculate the amount of money a sentence would cost before recommending it to a judge, and argue why the cost is justified. He estimates that it costs $115 a day, or $42,000 a year, to incarcerate one person. So, if a prosecutor seeks a three-year sentence, she must state, on the record, that it would cost taxpayers $126,000 and explain why she thinks this cost is justified. Krasner reminds his attorneys that the cost of one year of unnecessary incarceration “is in the range of the cost of one year’s salary for a beginning teacher, police officer, fire fighter, social worker, Assistant District Attorney, or addiction counselor.”

The same reasoning could be applied to just about any new rule or regulation introduced by government.

Comment?

This is a brief account of a lengthy 2014 dialogue I had with Patrick Whelan, a thoughtful architect in WA. You are now invited to join the discussion.

Patrick: In WA, a scoring model was devised and adopted for all police buildings, It scored building fabric condition and the condition of services to determine an overall condition score. The building’s suitability for purpose was then determined by comparing scores for compliance with the Building Code of Australia and for compliance with the Police Building Code (the agency’s accommodation standards) Comparing the Condition score with the Suitability score enabled a ‘works priority score’ for the station, in effect displaying a level of service offered by each station.

Penny: Whilst building condition and code compliance are important, they are important from the perspective of the building maintenance manager. To get at the idea of service perhaps we need to look at what the building user wants to get out of the building. A building may be in excellent condition and meet all code conditions, yet still fail to work efficiently for the user. It may be that the design is no longer suitable for the new work that needs to be carried out, or it may have the wrong capacity – either too much or too little. It may be in the wrong place!

Patrick: In the case of the WA Police, their Building Code articulates everything needed of a building to progress policing: Planning criteria, technical criteria, functional relationship diagrams, room data sheets, formulae for calculating room sizes and the number of ablutions facilities, guidelines for the compliant design of custodial facilities, etc. The Police, being a paramilitary organisation, have a very strong handle on what is needed to do the job. However, things change over time, and the building code changes with them.

Penny: Building codes are so efficient because, in the short term, people only need to respond, ‘on the dotted line’, as it were: they don’t have to think. However can what makes for short term efficiency lend itself to longer term ineffectiveness? What can be done to determine a code that is both efficient and effective?

Over to you!

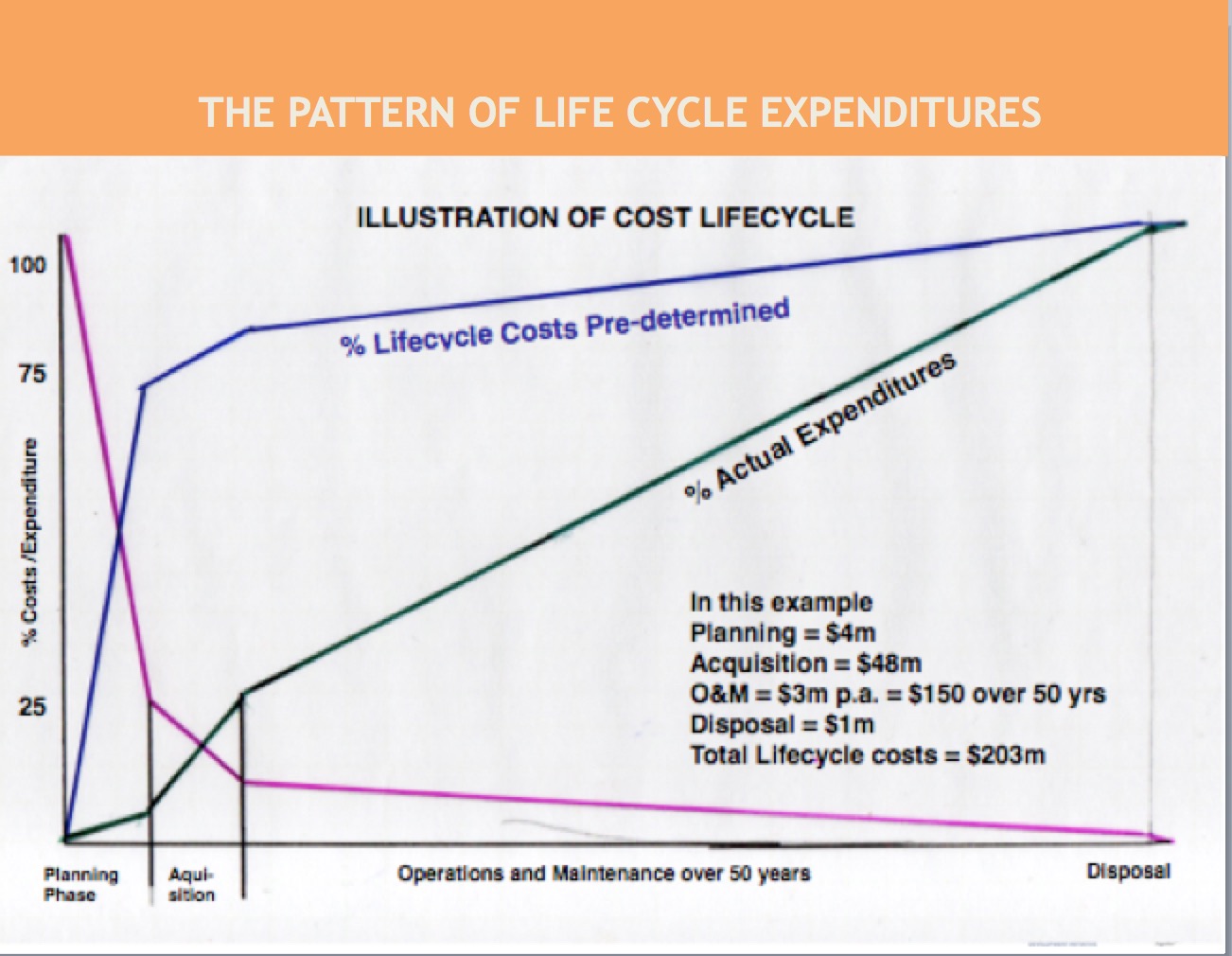

18 months ago I had the pleasure of co-designing and presenting a capacity building workshop for Auditors-General in the Pacific Islands. The subject of the workshop was auditing for the better management of public assets. We looked at the 4 stages – planning, construction,operations & maintenance and, finally, renewal or disposal – and discussion revealed that the auditors chose to spend the bulk of their time in analysing performance at the operations & maintenance stage. This made sense. It is by far and away the area where most expenses occur. However, it is not the stage where most expenses are committed. That occurs much earlier, at the planning stage. This is the stage where the nature, location and size of the project are determined and these are the primary determinants of how much will be spent later at the operations and maintenance stage.

I drew up a hypothetical schema to make the point. It showed that, by the end of the first or planning stage, only $4m of the total life cycle costs ($203m) had been spent BUT, the decisions made during this phase had already committed about 75% (and sometimes more) of the total costs. In the diagram the green line represents costs actually expended, the blue line costs pre-determined and the purple line represents the scope remaining to make a difference to total costs. This shows that by the time the plant is commissioned and operational, there is really relatively little that can then be done to improve on the overall life cycle costs.

The figures I used in this example are fictitious.

They are consistent with the theory and principles of life cycle costing as shown in the major textbooks on the subject.

I would have liked to use real figures but I couldn’t find any. So I contacted people who might be expected to know – key academic figures in asset management, experienced consultants, long time practitioners. But no, no-one could help.

So my question today is:

Why do we have so little actual data about this very key and critical stage of decision making? And how can we improve our knowledge – and thus our performance?

In the last post “The Infrastructure Quiz” I asked what the ‘purpose’ of infrastructure is. What did you choose? If you ask this question of most people, the answer is obvious – it just isn’t the same answer for everyone!

Have a look at the following possibilities:

- For asset managers, the answer is obvious – it is to provide needed services that underpin the economy and society well being.

- For economists in the Treasuries, the answer is equally obvious – it is to kickstart the economy. (For many years we had a stop-go policy for infrastructure. Whenever the economy got overheated, governments would cut back on infrastructure spending, and whenever it slowed down, they would spend more. There was a period in the early 2000s when this was recognised for the damage it caused. But now it seems to be back again.)

- Politicians and Think tanks are the ones likely to claim that infrastructure – ‘increases productivity’ and ‘raises the standard of living’ (but they seldom spell out exactly how, for it is all regarded as self-evident.)

- For the general public (most of whom could not give any examples of infrastructure beyond roads, if that) the answer is that the purpose of infrastructure spending is to ‘create jobs’.

- Military and strategic planners often see the construction and location of infrastructure as a strategic control problem. Many politicians do the same.

- The construction industry and its lobbyists strongly believe that we not only need infrastructure to keep the industry afloat but that we need to forecast what infrastructure and where in order to enable them to plan.

So, many purposes – all ‘self evident’!

Editor: You can find earlier posts on budgets, by using the search function, and all posts by Mark by selecting his name.

Further to my earlier posts about asset budgets, I couldn’t help but want to have another go at this by asking a slightly different set of questions. These relate to the principle of transparency.

Further to my earlier posts about asset budgets, I couldn’t help but want to have another go at this by asking a slightly different set of questions. These relate to the principle of transparency.

By transparency I mean:

Is there a clear and documented basis for the estimates upon which the asset budget has been based?

- Are the estimates based on ‘simple’ or ‘averaged’ projections of expenditure rather than ‘modelled’ projections that emulate realistic timings and patterns of expenditure for the nature of the works involved and how they will be procured?

- Is it based on estimates for all assets over the full period that the budget is meant to address? By all I really mean a schedule that lists all of the assets, including those for which a $NIL expenditure is forecast for the relevant period. (I ask this as a check that all assets have been given consideration.)

- Are the underlying assumptions documented and made clear to those being asked to approve the budget – especially the reliability / sensitivity of rates used and associated finance costs?

- Are the priorities inherent and sequencing / pace of the proposed works also made clear and demonstrably aligned with corporate business and services priorities for the forecast period? How does this align with projected cashflow requirements and funding availability? (A projection showing a skewed acceleration of expenditure towards the final quarter must raise concerns – not only about reliability of delivery, but also in relation to business and services priorities being effectively supported, and in relation to getting value for money from what is going to be spent.)

- Are the risks that are inherent to the portfolio and the proposed program delivery made clear and ‘current’ for the immediate and forecast context of the program and its delivery?

If these aspects are not transparent to the decision-makers then there is greater risk that the program will not be delivered and the budget will be nowhere near accurate

I am sitting in the dark, the temperature is 36 degrees Celsius. I have a radio and an iPad. I’d like to say that I’m on holiday in the tropics, but I’m in my home in the outskirts of a city and the power has been out for a 6 hours now. I’m a Telstra customer, but there is no mobile or landline service – batteries not included in their infrastructure apparently. If I were part of a local generating group I would be cool and communicating. If my group had a similar power failure I would be drawing from other interconnected communities.

I am sitting in the dark, the temperature is 36 degrees Celsius. I have a radio and an iPad. I’d like to say that I’m on holiday in the tropics, but I’m in my home in the outskirts of a city and the power has been out for a 6 hours now. I’m a Telstra customer, but there is no mobile or landline service – batteries not included in their infrastructure apparently. If I were part of a local generating group I would be cool and communicating. If my group had a similar power failure I would be drawing from other interconnected communities.

My question is – who has heard of the 3rd industrial revolution, and has anyone seen a recent advance toward it in Australia?

The value of “value management”, as Mark Neasbey, Director of the Australian Centre for Value Management, has illustrated in each of his previous posts, is in challenging what we think we know. In “The Power of ‘What if?'” he reveals how questioning a ‘given’ led to a radically different solution and a saving of hundreds of millions of dollars. Mark writes:

The value of “value management”, as Mark Neasbey, Director of the Australian Centre for Value Management, has illustrated in each of his previous posts, is in challenging what we think we know. In “The Power of ‘What if?'” he reveals how questioning a ‘given’ led to a radically different solution and a saving of hundreds of millions of dollars. Mark writes:

The types of things that are generally in a list of givens include:

- a law or regulation that has to be complied with;

- a technical performance requirement – be it a range or a set minimum or maximum number or a specific number – which can represent dimensions, volumes, rates and so on;

- a limiting boundary or barrier or a technical constraint;

- financial – e.g. an amount not to be exceeded or specified sources of funding, interest rates and so on;

- ownership and operating arrangements;

- authorities and delegations;

- a specific time or date that the asset is required or to be disposed of; and

- application of a particular process or corporate policy.

[Not an exhaustive but just some main examples.]

Now the thing about such givens is that we develop our options or solutions accepting these, rather than challenging them. So they tend not to come into creative thinking processes, accept as a limitation. Yet what happens if its not really a given, rather it turns out to be possible to change it – even if only to treat it as an assumption?

A recent rail project to develop expanded train maintenance and stabling facilities began with a given that the existing mainline was fixed – it could not be changed. By not allowing it to be moved the project solution involved some complex and expensive engineering and infrastructure to manage the train movements into and out of the depot, which are planned to eventually have headways as short as 30 seconds. [Driverless trains.] There was also an effect on how the layout of the expanded facility could be realised – it was not going to be as ideally efficient as possible to operate.

During a value engineering review however, the effects of not moving the mainline to the engineered solution became clearly a cause – not of concern – but for a better appreciation of the opportunity forgone to create a simpler, more elegant engineered solution and at a huge cost reduction.

The mainline alignment had been stated as a given by the client early in the planning process. So all of the initial feasibility work and preliminary concepts evolved based on that given. What subsequently emerged in the value engineering review was that this arose from a decision not to acquire a particular developed property adjacent to the line.

By asking the simple question “what if…?” the team was able to show a much better outcome was possible – not only at a lower capital cost, but with significant long term reduction in maintenance and operational risks to the network.

Two important highlight lessons to me are:

- Do you have an understanding of what is being labelled or taken as givens for your assets and asset strategies?

- Do you have a process to all testing and challenging of such givens so decision-makers are aware of their implications?

The Task today: An answer to either of Mark’s questions OR an example of a positive ‘What if?” challenge of your own.

This is the fourth of a series of posts by Mark Neasbey, a director in the Australian Centre for Value Management examining the role of the planning budget. In the first Mark considered the differing attitudes that may be taken to strict adherence to the budget and in the next two, he gave examples of the problems this had created for a major teaching hospital and for a mining operation. In this, the last of the present series, Mark considers how a planning budget can be constructed and utilized to smooth the path of the capital budget.

This is the fourth of a series of posts by Mark Neasbey, a director in the Australian Centre for Value Management examining the role of the planning budget. In the first Mark considered the differing attitudes that may be taken to strict adherence to the budget and in the next two, he gave examples of the problems this had created for a major teaching hospital and for a mining operation. In this, the last of the present series, Mark considers how a planning budget can be constructed and utilized to smooth the path of the capital budget.

It’s good business practice to require planning for asset projects to look well ahead of the short-term i.e the current financial reporting period. This is because assets typically last many years and impose long-term costs to the business or government service.

Good practice also involves life-cycle planning around the asset project – what it costs to establish, what needs to be spent to keep it operating, periodic costs for replacement and renewal of plant and equipment and also periodic refurbishment necessary to sustain functionality, safety, image etc. This extends to considering disposal – when an asset is no longer needed – what has to be done to get rid of it. This principle applies equally to physical assets and soft assets such as computer software or systems.

So when an initial concept is proposed, what sort of things need to be addressed and what’s the significance of these to the budget?

Well a key starting point has to be determining its purpose – what is the asset supposed to do? What are the business or service functions that the asset must accommodate or support? Why can’t these functions be undertaken some other way, without the need for the asset project?

These questions can’t be answered without research, we need to test and clarify the scope of the project so we can set a reasonable capital budget. That means we have to start with a planning budget so the planning and analysis work can be done to decide a) the functions that the organisation needs to deliver; b) the options that should be considered for delivering those functions – including non-asset strategies; c) determine the relative merits of the options – key pros and cons, including business (service delivery) risks.

Recent Comments